You have debt.

Siguro hindi pa sobrang lala and maybe you can still pay it. Pero overwhelming na.

Kapag nakikita mo ‘yung mga bills mo, ‘yung due dates, ‘yung notifications mula sa GCash o sa bangko, you feel the weight of it. You’re slowly drowning from everything at laging umiikot sa isip mo kung paano mo babayaran lahat ng utang mo.

Kung nakaka-relate ka rito, this newsletter is for you. But before we get into the tips, let me address the real problem first.

The Problem Isn’t The Debt. It’s Your Mindset About It

Maraming Pilipino ang ganito mag-isip pag dating sa utang:

- “Okay lang naman ‘yan. Lahat naman may utang eh.”

- “Kikitain ko rin naman ‘yung pambayad next month.”

- “Deserve ko naman ‘to. Nagpakahirap akong mag-work para dito.”

Does it sound familiar? Look, I’m not here to judge you. On the contrary, sinulat ko nga ‘to para makatulong sayo. I’ve been where you are now. Naramdaman at naisip ko rin ‘yang mga bagay na ‘yan. But by God’s grace, nakalabas din ako d’yan.

Here’s the truth: ‘yung mga beliefs na ‘yan, they are not helping you. Nakakalason sila at pinatapatay nila ang financial future mo. Bakit? Kasi ginagawa nilang normal ang isang bagay na hindi dapat normal. Debt enslaves us. Pero ang will ng Diyos sa’tin ay maging free tayo.

The Bible says it plainly in Proverbs 22:7: “The rich rules over the poor, and the borrower is the slave of the lender.”

Now, hindi ‘to sinasabi ng Bible para takutin tayo. It’s a warning: ‘yung utang, kahit gaano kaliit, kahit gaano ka-manageable ‘yan, may hawak ‘yan satin. Hindi lang financially, but spiritually as well. It holds our freedom. And you know what’s the best way to stay free? ‘Yung ‘wag nating hayaan na lumalim pa ‘yung hawak satin ng utang.

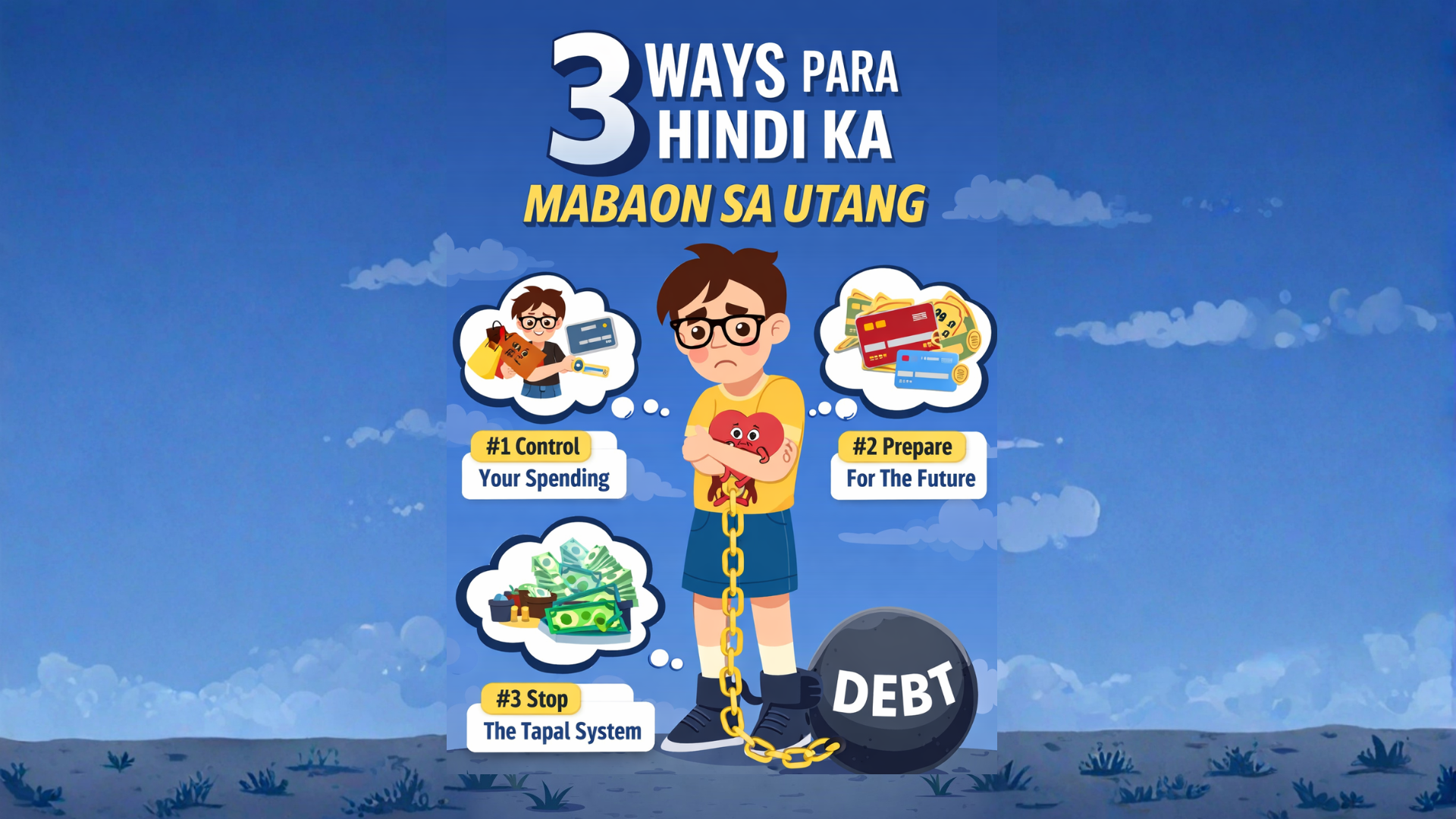

So let’s talk about the three ways para hindi mabaon sa utang. Because it’s so much easier to avoid debt than to escape it once you’re already drowning.

#1: Control Your Spending

Let me ask you a question: Bakit ka nagkaroon ng utang?

In most cases, hindi dahil maliit ang sweldo mo. Hindi dahil mahal ang bilihin at sobrang mahal ng gastos para mabuhay tayo. The reason why we get into debt is because lumalagpas ang gastos natin sa kinikita natin.

I know this because it happened to me.

Nung nagkaroon ako ng first job ko, first time ko ring magkaroon ng regular na pera. And you know what I did? Ginastos ko lahat sa pagkain, sapatos, damit, pang-date, at iba pa. ‘Yung tipong, wherever the money was, that’s where my spending was too. Nag-enjoy ako. Pero wala akong naiipon. And if I had an emergency back then? Malamang nalubog din ako sa utang.

That’s the danger of lifestyle inflation. At hindi mo mararamdaman ‘yun hanggang hindi mo na kaya.

Here’s the thing: a lot of us use debt to afford the lifestyle we want, not the lifestyle we can actually sustain. Imagine, we swipe our credit cards para sa bag. We buy gadgets we can’t afford through installments. Tapos sobrang daming tumatangkilik sa “Buy now, pay later” na scheme ng mga companies.

And the data backs this up. According to the BSP’s Consumer Expectations Survey, only 25.6% of Filipino households reported having savings as of Q4 2024. That’s the lowest level in over three years. Ibig sabihin, almost 3 out of 4 Filipino households ang walang savings. In short, gumagastos muna sila tapos kung may matitira man, tsaka na lang mag-iipon. Pero madalas, walang naiipon.

That’s the pattern and it’s exactly what leads people deeper into debt.

So here’s what you can do:

- Step 1: Track where your money actually goes. Before you budget, you need to know where the money is bleeding out. The best way to do that is to track your expenses for at least 30 days. Lahat isasama mo, kahit ‘yung P50 na merienda.

- Step 2: Save first, spend what’s left. Kapag natanggap mo ang sweldo mo, maglagay ka agad ng pera sa savings mo at para sa pangbayad ng utang. Tapos, you’ll spend the rest. We have to flip the script para makalabas sa utang ng mas mabilis.

- Step 3: Make it harder to spend impulsively. Remove your saved credit card details from shopping apps. Delete the apps that tempt you most. Kapag kasi hassle, ‘di na natin ginagawa. So, use that to help yourself by making spending inconvenient.

Grab A Copy Of This FREE eBook + Video Training

Discover the 5 WORST MISTAKES people do that keeps them in debt (and how to solve it)

#2: Prepare For The Future

Isipin mo ‘to: What actually happens to most people na nagkakaroon ng utang?

Now, I’m aware that there are multiple reasons why people get into debt. It’s not always because of extravagance or lifestyle inflation. Sometimes, this is the story: May family emergency ka. Nagkasakit ‘yung isa sa mga mahal mo sa buhay. Nawalan ka bigla ng trabaho. Nasiraan ka ng sasakyan. And in all those, wala kang emergency fund. So naturally, magkakaroon ka ng utang to get out of that.

This is a common cycle na nakikita ko sa mga taong nagshe-share sakin ng utang problems nila both personally and on social media. And the heartbreaking part? Preventable siya.

Sabi sa Proverbs 22:3, “The prudent sees danger and hides himself, but the simple go on and suffer for it.”

Preparing for emergencies isn’t being paranoid. It’s you being wise and grounded in reality that life happens.

But how do we prepare for the future? Here are 2 things you can do:

- 1: Build your Emergency Fund (or “Peace of Mind Fund”). Usually, ang formula is 3 to 6 months of your monthly expenses. Kung ang gastos mo ay ₱15,000 a month, your target is ₱45,000 to ₱90,000. Tapos dapat nasa separate account ‘to at hindi mo gagalawin unless it’s a real emergency. Ito kasi ‘yung first line of defense mo eh. Kapag may emergency kang naranasan, hindi mo na kailangan pang mangutang.

- 2: Know your Financial Freedom Number. ‘Yung emergency fund natin is just the beginning. Long term, we need to know our target. Your Financial Freedom Number is the total amount of investments you need so that the returns alone can cover your living expenses. Meaning, kahit hindi ka na mag-trabaho, sapat ‘yung kinikita ng investments mo para buhayin ka.

Now, hindi mo kailangang maabot ‘to agad. But you need to know where you’re going.

#3: Stop The Tapal System

Okay. This one’s a bit uncomfortable to talk about pero kailangan nating pag-usapan. Have you ever experienced this scenario? May utang ka sa Credit Card A tapos due date na. Ang problema, wala kang pambayad. So, you borrow from a friend or you take out a loan from another app para makabayad ka. Tapos next month, imbes na isa lang ang utang mo, dalawa na. Tapos tatlo. Tapos apat. And the cycle keeps going.

That’s the tapal system: uutang para makabayad sa utang. Here‘s the sad part: alam nating hindi ito solusyon. But we keep doing it anyway. Bakit? Because it gives you temporary stress relief. Naa-address ‘yung due date at natatanggal ‘yung anxiety. For now. Pero hindi siya long-term solution.

You know, our brain naturally looks for the easiest and fastest relief available. And the tapal system? It’s fast! But here’s the kicker: lalo mo lang nilulubog ang sarili mo. You’re not paying off debt, you’re just moving it around plus interest. Patong-patong na interest. Ang ending, mas malaki pa ang utang mo kaysa nung una.

And that, my friend, is exactly what the data shows. According to TransUnion‘s Consumer Pulse Study, 42% of Filipino respondents struggled to pay their bills and loans in full. That number hasn’t improved from the previous years. Isipin mo ‘yun? Almost half are stuck in debt and that’s why they do the tapal system.

So here’s what to do instead:

- Step 1: List down ALL your debts. Write down the name of each creditor, the amount you owe, and the interest rate. Kailangan mong makita ang buong picture bago mo ‘to malagpasan.

- Step 2: Pick a payoff strategy. Is it Debt Snowball or Debt Avalanche? Any of these two is better than the tapal system. Both of them work. Kailangan mo lang mamili ng strategy na magwo-work sayo.

- Snowball Method: Pay off the smallest debt first. Then roll that payment toward the next one. It’s great for motivation and momentum.

- Avalanche Method: Pay off the highest-interest debt first. It saves you more money in the long run.

- Step 3: Don‘t create new debt while you‘re paying off old ones. Ito ang pinakamahirap na part. Habang nagbabayad ka, huwag mo na munang dagdagan ‘yung utang mo. You can’t get out of the hole if you don’t stop digging.

Here‘s The Most Important Thing I Want You To Remember

Let’s go back to what I said at the start—it‘s so much easier to avoid debt than to escape it once you’re already buried. This isn’t an exaggeration. It’s the truth. And right now, while you still have the ability to pay, while you’re not yet fully buried, this is the right time to act.

Not tomorrow. Not ‘pag may “extra” na ako. Now is the best time to act.

So here’s a quick recap:

- Control your spending. Track where your money goes, save first before spending, and make impulse buying inconvenient.

- Prepare for the future. Build your emergency fund and start thinking about your long-term Financial Freedom Number.

- Stop the tapal system: list all your debts, pick a payoff strategy, and don’t add new debt while paying off old ones.

Now, hindi ‘to madaling gawin ah? It’s easier said than done. But it’s the right thing to do. And that, my friend, is how you stay free.

Just conquer today,

Jeric Timbang